The Marketing Minute: Marketing With Layers

The Marketing Minute: Marketing With Layers The Right Approach: Electro-Tek—A Williams Family Legacy, Part 1

The Right Approach: Electro-Tek—A Williams Family Legacy, Part 1 It’s Only Common Sense: If You’re Not Differentiated, You’re Dead

It’s Only Common Sense: If You’re Not Differentiated, You’re Dead

Next-generation Memories Have a Chance to Penetrate into the Market in 2020

May 20, 2019 | TrendForceEstimated reading time: 2 minutes

Whether DRAM or NAND Flash, current memory solutions are straining the physical limits of production processes, meaning it is becoming more and more difficult to keep on raising performance and lowering costs. Therefore, there has been much discussion revolving around Intel Optane and other next-generation memories in recent years, in hopes of discovering new solutions while keeping modifications to the current platform to a minimum or even leaving it completely untouched. DRAMeXchange , a division of TrendForce , holds that next-generation memories and current solutions have their respective pros and cons, with prices forming the most critical areas of opportunity.

TrendForce states that Intel, Samsung and Micron and other memory manufacturers have already began investments into next-generation memory solutions such as MRAM, PRAM and RRAM. Intel's Optane, for example, uses 3DxPoint as the basis for designing server products. Since the release of DIMMs, which are completely compatible with servers on the market, identical slots allow motherboard design manufacturers to change server modules or Optane solutions at will to control the total cost of the completed product.

However, next-generation memory costs remain high due to the lack of up-scaling and normalization, leading vendors to target datacenters and other special applications, especially hyperscale datacenters with rather highly customized designs, which will allow new configurations to be planned for different memories.

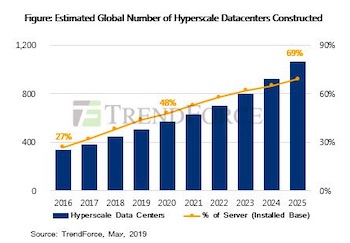

Due to AI reaching maturity and the pervasiveness of intelligent end devices in recent years, many application services have been integrated through the use of servers, especially those application services which require a huge amount of data for computation and training. Furthermore, server demand has been on the rise as virtual platform and cloud storage technologies gradually develop, bringing about the growth of hyperscale datacenters in the process. According to TrendForce's investigations, the number of hyperscale datacenters constructed globally will reach a projected 1070 in 2025, registering a CAGR growth of 13.7 % over the 2016-2025 period.

Memory Prices to Bounce in 2020, Forming an Area of Opportunity for Next-generation Memories

From a market standpoint, DRAM and NAND are all facing oversupply, and current memory solution prices remain at a low point. The continual descent in DRAM prices is basically due to the drop in server and smartphone demand and the consequent quick-freeze in consumption and accumulating inventories. The NAND market, on the other hand, is prone to wars over market shares, and the shift from 2D NAND to varying degrees of 3D NAND caused supply bits to grow by large. In summary of the above, DRAM and NAND prices slid simultaneously and speedily in 2019, and NAND prices are nearing cash costs for suppliers.

Due to the cheapening trend of existing memory solutions, it may not be the best time for next-generation memories to make their entrance. Yet restocking momentum built through the gradual recovery in demand and price flexibility may occasion a rebound in server price in 2020, giving next-generation solutions a better chance to penetrate into the market. TrendForce posits that in the future years to come, there will be more adoption of next-generation memories in the market, allowing them to become alternative solutions.

About TrendForce

TrendForce is a global provider of the latest development, insight, and analysis of the technology industry. Having served businesses for over a decade, the company has built up a strong membership base of 435,000 subscribers. TrendForce has established a reputation as an organization that offers insightful and accurate analysis of the technology industry through five major research divisions: DRAMeXchange, WitsView, LEDinside, EnergyTrend and Topology. Founded in Taipei, Taiwan in 2000, TrendForce has extended its presence in China since 2004 with offices in Shenzhen and Beijing.

Share on:

Testimonial

"Our marketing partnership with I-Connect007 is already delivering. Just a day after our press release went live, we received a direct inquiry about our updated products!"

Rachael Temple - AlltematedSuggested Items

The Marketing Minute: Marketing With Layers

10/15/2025 | Brittany Martin -- Column: The Marketing MinuteMarketing to a technical audience is like crafting a multilayer board: Each layer serves a purpose, from the surface story to the buried detail that keeps everything connected. At I-Connect007, we’ve learned that the best marketing campaigns aren’t built linearly; they’re layered. A campaign might start with a highly technical resource, such as an in-depth article, a white paper, or a podcast featuring an engineer delving into the details of a process. That’s the foundation, the substance that earns credibility.

ICT Symposium Review: Sustainability and the Circular Economy

10/09/2025 | Pete Starkey, I-Connect007It was pleasant autumnal weather as we made our way once again to Meriden, the nominal centre of England, for the 2025 Annual Symposium of the Institute of Circuit Technology. Delegates were welcomed by technical director Emma Hudson who introduced and moderated a skilfully coordinated programme, focused on the highly relevant theme of sustainability.

Circular Packaging Market to Reach $98.0 Billion by 2035

10/08/2025 | Fact.MRThe market's journey from USD 45.8 billion in 2025 to USD 98.0 billion by 2035 represents substantial growth, the market will rise at a CAGR of 7.9% demonstrating the accelerating adoption of sustainable packaging systems and circular economy solutions across food & beverage, personal care, and e-commerce sectors.

It’s Only Common Sense: Stop Whining About the Market—Outwork It

10/06/2025 | Dan Beaulieu -- Column: It's Only Common SenseWhenever the market hiccups or the industry cycle dips, I hear the same tired chorus: “The market is down. Customers aren’t buying. What can we do? We just have to wait it out.” Nonsense. If you think that by showing up, opening your doors, and waiting for the economy to smile kindly upon you, that success will follow, you are in the wrong business. Worse yet, you’re living in the wrong mindset. Most people don’t want to hear the truth that winners find business in down cycles. Losers blame the economy.

Schweizer Ends Staff Restructuring Measures and Short-Time Working at the Schramberg Site

10/01/2025 | Schweizer Electronic AGSchweizer Electronic AG has implemented comprehensive measures to adjust its cost and personnel structure at its Schramberg site due to strong market fluctuations in the automotive and industrial electronics sector. Thanks to the successful restructuring, short-time working can now be ended with immediate effect. A stable order situation is expected for the fourth quarter, with signs of growth momentum returning in 2026.