It’s Only Common Sense: Stay Curious, My Friends

It’s Only Common Sense: Stay Curious, My Friends The Marketing Minute: AI Is Watching Your Marketing Habits

The Marketing Minute: AI Is Watching Your Marketing Habits

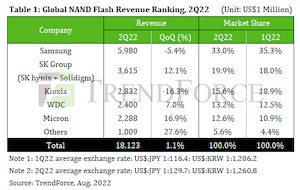

According to TrendForce research, NAND Flash contract pricing increased by approximately 3-8% in 2Q22 due to Kioxia’s raw material contamination incident. However, consumer demand remained sluggish, resulting in weaker bits demand in laptops, chromebooks, TVs, and smartphones and leading to a rise in client inventory levels. Enterprise SSD purchasing has maintained strong momentum, offsetting sluggish consumer demand. In 2Q22, supplier bit shipments decreased by 1.3% QoQ, while ASP increased by 2.3%. Overall NAND Flash industry revenue reached US$18.12 billion, growing 1.1% QoQ.

Since consumer demand is weak, the slump in shipments has offset demand for mobile NAND Flash even though average smartphone capacity is still growing. At the same time, PC customers continue to lower their shipment expectations, resulting in flat shipments of client SSDs. In contrast, server shipments are booming while a backstop remains for enterprise SSD demand from data centers, though the overall situation caused Samsung's 2Q22 bit shipments to decrease by nearly 10%. However, thanks to exchange rates and high-capacity products, the company’s product mix improved, driving NAND Flash ASP higher and pushing revenue to US$5.98 billion, down 5.4% QoQ.

SK Group (SK hynix & Solidigm) strengthened its partnerships with North American clients in 2Q22 and successfully increased the proportion of SSD product shipments post-raw material contamination incident, which helped SK hynix’s growth performance this quarter. Strong demand for servers also led to growth in Solidigm's enterprise SSD shipments, resulting in SK Group's consolidated NAND bit shipments growing nearly 10% QoQ. NAND Flash ASP was also boosted by product mix synergy. In total, SK Group's NAND Flash revenue in 2Q22 increased by 12.1% QoQ to US$3.61 billion.

Due to its raw material contamination incident at the beginning of the year and loss of output caused by pandemic-related closure of auxiliary packaging and testing facilities, Kioxia's bit shipments fell by more than 20% in 2Q22. However, ASP increased thanks to exchange rates and strong shipment performance of enterprise SSD. Kioxia’s total 2Q22 revenue came in at US$2.83 billion, falling 16.3% QoQ. The company’s revenue market share fell to third place.

Western Digital's 2Q22 bit shipments grew 6% QoQ and its NAND Flash division revenue was US$2.40 billion, up 7.0% QoQ. Enterprise SSD revenue doubled and the proportion of high-priced products increased, resulting in a 2% QoQ increase in overall ASP. Western Digital posted good SSD revenue performance in this quarter. In addition to enterprise SSD, bit shipments of gaming SSD also increased by 70% YoY. At the same time, the company was certified as a supplier for Sony’s PS5.

Micron benefited from heightened purchasing from PC OEM customers in response to the raw material contamination incident and strong demand from data center customers. Its chief TLC and 96L products drove the growth of enterprise SSD shipments in 2Q22. The company also gained more market share in the client SSD segment, pushing up 2Q22 NAND Flash revenue by 16.9% to US$2.29 billion, a record high. Bit shipments grew approximately 17-19%, while ASP dropped slightly by nearly 1%.

Looking at 3Q22, TrendForce indicates that rising inflation, the Russian-Ukrainian war, and the pandemic will continue to depress market demand and lead to a disappointing peak season. Since oversupply continues to fester, the supply chain is expected to aggressively destock in 3Q22, leading to product dumping. NAND Flash contract pricing is expected to fall by 13-18% and overall revenue is expected to drop by 10% QoQ.