Standard of Excellence: Turning Negative Customer Feedback Into Positive Outcomes

Standard of Excellence: Turning Negative Customer Feedback Into Positive Outcomes Smart Automation: The Growing Role of Additive Manufacturing

Smart Automation: The Growing Role of Additive Manufacturing Global Citizenship: Redefining Connection and Responsibility in Digital Transformation

Global Citizenship: Redefining Connection and Responsibility in Digital Transformation

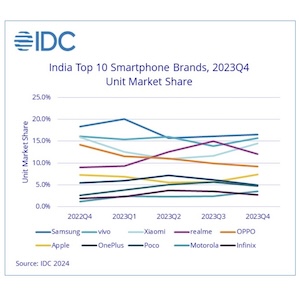

India’s Smartphone Market Grew by 1% YoY in 2023 to 146 Million Units

February 13, 2024 | IDCEstimated reading time: 4 minutes

According to the International Data Corporation ’s (IDC) Worldwide Quarterly Mobile Phone Tracker, India’s smartphone market shipped 146 million smartphones in 2023, with a nominal 1% growth YoY (year-over-year). The second half of the year grew by 11% YoY in 2H23, compensating for the sharp 10% decline in the first half. 4Q23 grew by 26% YoY with shipments of 37 million units, as the second half of the quarter saw stronger than expected shipments with several new model launches.

Consumer demand remained stressed, leading to excess inventory levels across channels despite price corrections and schemes by the vendors. At the same time, the ASP (average selling price) hit a record of US$255, rising 14% YoY in 2023. This also marks the third consecutive year of double-digit ASP growth restricting smartphone market recovery. The high ASP can be attributed to the increasing share of the premium-segment (US$600+) from 6% in 2022 to 10% in 2023, along with a rapid uptake in 5G shipments to a record 55% share.

“Most brands chose to reduce prices and offer additional channel margins in the last quarter to manage the inventory levels from post festive cyclic dip. This will give a lukewarm start to 2024 with cautious stocking by the channels,” said Upasana Joshi, Research Manager, Client Devices, IDC India.

Key Highlights for 2023:

- Shipments to online channels dropped by 6% and its share dropped to 49% in 2023, down from 53% in 2022. Offline channel shipments grew by 8% YoY as vendors strengthened their retail presence with lucrative premium offerings as well as an expansion into smaller towns and cities.

Price segment details:

The entry level (sub-US$100) segment grew by 12% YoY to 20% share, up from 18% a year ago. While Xiaomi continued to lead, POCO (2nd) and Samsung (3rd) emerged in the top brand list.

Shipments to the mass budget (US$100<US$200) segment declined, with its share dropping to 44% from 51%, declining by 12% YoY. vivo, Realme and Samsung together accounted for 53% of shipments.

The entry-premium (US$200<US$400) segment remained flat, with 21% share. vivo and OnePlus had significant share, making up almost 40% of overall shipments in this price segment.

The mid-premium segment (US$400<US$600) reached a share of 5%, growing by 27% YoY. OnePlus continued to lead with 35% share, followed by Samsung and vivo.

The premium segment (US$600<US$800) reached 3% share, growing by 23%, led by the iPhone 13, Galaxy S23/S23 FE and OnePlus 11. While Apple’s share declined, Samsung’s share more than doubled in this segment.

The super-premium segment (US$800+) registered the highest growth of 86%, with its share up from 4% to 7%. The iPhone14/13/14 Plus together accounted for 54% of shipments, followed by the Galaxy S23+/S23/S22+/S23 Ultra with 22% share. Overall, Apple led the segment with a share of 68%, followed by Samsung at 30%.

- 79 million 5G smartphones shipped in 2023, with a plethora of launches in the mass budget segment. 5G ASPs dropped to US$374, a decline of 5% YoY in 2023. Within 5G shipments, the mass budget (US$100<US200) segment share increased to 35% from 22% a year ago, while the entry-premium (US$200<US$400) segment continued to dominate with 38% share, albeit down from 49% in 2022. Apple’s iPhone 13 & 14, Samsung’s Galaxy A14, vivo’s T2x and Xiaomi’s Redmi12 were the highest shipped 5G models in 2023.

- Almost a million shipments of foldable phones shipped, with ASPs declining by 4% at US$1,236. Samsung led the foldable phone market, although its share dropped to 73% in 2023 as other players such as Motorola, Tecno, OnePlus and OPPO have entered India’s foldable market.

- The share of MediaTek-based smartphones increased to 50%, growing by 6% YoY. vivo’s T2x, Xiaomi’s Redmi A2, and Realme’s C55 were the highest shipped MediaTek-based models. Qualcomm’s share dropped to 25%, a shipment decline of 6% YoY.

Brand performance

Apple had a stellar year, finishing at 9 million units, despite having the highest ASP of US$940. This was led by previous generation iPhone models and its push for local manufacturing. Its iPhone 13/14 were amongst the Top 5 shipped models annually.

As a brand, Samsung remained in the leadership position, with a record high ASP of US$338, although with a 5% shipment decline YoY. Its Galaxy A14 was the highest shipped device of 2023.

vivo (excluding iQOO) climbed to the second slot as shipments and ASPs both grew by 8% and 9% respectively. It was the only brand to register growth amongst the top five brands.

Realme, despite facing challenges in the beginning of the year, maintained its third position, led by affordable launches.

- After declining for four consecutive years, 61 million feature phones shipped, growing by 8% YoY. While Samsung exited the feature phone segment, Transsion continued to lead, followed by Lava. The entry of Reliance Jio’s new 4G feature phone fueled growth in 2H23.

“The road to recovery for smartphones in 2024 looks strained and elongated, as worries around income, inflationary stress, price increases, and inventories remain. 2023 was all about affordable 5G devices, timely price corrections, and offline channel expansion by brands, whereas 2024 and beyond requires greater efforts, especially at entry-level price points, to fuel organic growth," says Navkendar Singh, AVP, Client Devices Research, IDC India.

“IDC estimates a flat to low single digit annual growth in 2024, primarily led by upgraders in (US$200<US$400) segment, backed by financing schemes, extended warranties and upgrade programs,” ends Singh.

Share on:

Suggested Items

TRI at SMTA Wisconsin Expo 2025

04/24/2025 | TRITest Research, Inc. (TRI), the leading test and inspection systems provider for the electronics manufacturing industry, will join the SMTA Wisconsin Expo 2025.

Driving Sustainability in PCB Design

04/24/2025 | Marcy LaRont, I-Connect007Filbert (Fil) Arzola is an electrical engineer at Raytheon. He’s smart, entertaining, and passionate about PCB design. As it turns out, he’s also passionate about “Mother Earth,” as he calls her. Born and raised in Southern California, he freely admits that he turns the water off when he brushes his teeth and yells at his brother for throwing batteries in the garbage. But when looking at the issue of sustainability and PCB design, he urges his audiences to ponder what sustainability looks like. Can PCB designers, he asks, make any impact on sustainability at all?

Real Time with... IPC APEX EXPO: Silicon Geometry's Signal Integrity Impact on PCBs

04/24/2025 | Marcy LaRont, I-Connect007At IPC APEX EXPO 2025, Kris Moyer addressed the importance of understanding the impact of silicon geometry reduction on signal integrity and PCB performance. Kris says signal integrity considerations are necessary for so many designs today, regardless of clock frequency. He discusses valuable insights from attendees regarding embedded resistor technology and the effects of radiation on smaller silicon features in aerospace applications.

Recognizing the IPC Committee Volunteer Awards in 2025

04/24/2025 | Patty Goldman, I-Connect007In 2023, IPC created two new awards to honor standards development committee volunteers: The Hillman-Lambert Award for Volunteer of the Year and the Kessler-Goldman Award for Committee Leader of the Year. The awards were named after Hall of Fame members whose service to standards development is well-known and who have demonstrated the skills and principles that the awardees should also have.

Explore Thermal Management Solutions in Latest Podcast Series—New Episode Now Available

04/23/2025 | I-Connect007I-Connect007 is excited to share the latest episode in our new podcast series! In this episode, Ryan returns to discuss practical strategies for managing heat, starting early in the design planning and specification phases. After all, prevention means there’s less to mitigate later.