The Chemical Connection: Onshoring PCB Production—Daunting but Certainly Possible

The Chemical Connection: Onshoring PCB Production—Daunting but Certainly Possible It’s Only Common Sense: The Phone Is Still Mightier Than the Keyboard

It’s Only Common Sense: The Phone Is Still Mightier Than the Keyboard

The Inverter Industry in China: Local Players are Gradually Becoming Unavoidable

June 3, 2016 | Yole DéveloppementEstimated reading time: 4 minutes

Chinese players have become leaders in diverse inverter market segments, forcing foreign players to collaborate with each other. The rail traction leader was created by the merger of CSR and CNR to form CRRC, which controls more than 40% of the market. Goldwind has become leader of the wind turbine market, dethroning historical leaders such as Vestas and GE for the first time. And while SMA has kept its number one position in the PV inverter market, both Sungrow and Huawei had better results in terms of new installed capacity in MW …

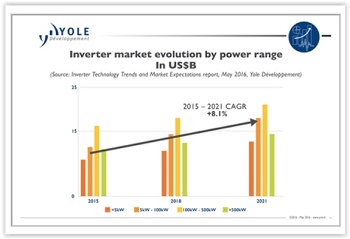

Yole Développement (Yole) proposes an overview of the Chinese inverter industry in its latest technology & market analysis, entitled Inverter Technology Trends & Market Expectations. This report explores the entire inverter market at all the steps along its supply chain. It analyzes the key market drivers that will shape this market in the future and provides a value-added understanding of the main technological challenges. With 6% growth between 2015 and 2021, the Chinese inverter industry must now deal with unavoidable Chinese companies.

Competition is intense in the global inverter market. In several market segments, over 40% of the inverters’ final destination is China, where Chinese suppliers have complete control (thanks to the Chinese government’s protection policies). Under this context, Chinese players have a huge opportunity to expand their activities and lead the inverter industry, even though within some market segments, they still have difficulty gaining market share outside China.

To resolve that situation, foreign players must now obtain or set up partnerships with competitors: thanks to powerful collaborations, they can compete with Chinese giants that come to the market with competitive prices.

This consolidation is already happening in the wind market with GE’s acquisition of Alstom’s renewables business in 2014 and the current discussions between Siemens and Gamesa. In the rail industry, discussions are ongoing in order to reinforce the position of European and American players. Within the EV/HEV industry, competition is fierce and local players, mostly focused at system and inverter level, control the market.

Analysts from Yole explore the Chinese inverter industry and highlight the specificities of this market and local players’ strategy:

- Under the wind turbines industry, China is showing an impressive expansion with over 30 GW installed, doubling its capacity compared to 2014 figures. Before 2005, foreign brands dominated the Chinese market, with more than 70% of market shares. Today the Chinese players dominate the wind turbine manufacturing market for local market. However, from the power electronic converters side for wind turbine applications, the situation is different: more than 50% of the converters are still imported from outside China. And, step by step, thanks to government policies, local manufacturers including Sungrow and CRRC are gaining market shares. Within the PV sector, Chinese inverters manufacturers expand their activities and consolidate their market position; Sungrow and Huawei took over the historical leader SMA for the first time in 2015(installed capacity). Nevertheless, in terms of revenues, SMA is still the leader. The Chinese government has an ambitious target of 150 GW of PV capacity by 2020. So far, it has some grid connection issues and targets are not being respected. But Yole highlights the impressive the PV capacity installed year after year in China.

- In parallel the rail market is dominated by four major players, all with a worldwide presence: Alstom (France), CRRC (China), Siemens (Germany) and Bombardier (France). With the emergence of CRRC (CSR and CNR fusion), the Asia area now plays in the big leagues, competing with the 3 other historic leaders.

- UPS market is also showing a great expansion in China. The Chinese market was reaching US$740 million in 2014, announces Yole in its inverter analysis.

- "The EV/HEV is today the most important market segment for inverters development”, says Mattin Grao Txapartegi, Technology & Market Analyst at Yole. “And China’s influence on the local EV market is inescapable: 2 of the 5 leading companies for BEVs and PHEV are Chinese: BYD and Renault Nissan.” Meanwhile, car makers are trying to go downward in the supply chain, aspiring to produce the entire powertrain. The automotive supply chain is large and complex in China, with many players from different fields, with different expertise. Thus, some energy companies are positioning themselves at the car inverter level creating new inter-application synergies. For example, the German company Siemens, which is already present in the energy, power generation and rail markets, recently revealed its willingness to enter the automotive industry with its own inverters product range.

To reinforce their market position and increase their revenues, Chinese companies expand their activities by addressing new market segments. The vertical integration is one of the main specificities of the inverter market in China. Yole’s analysts identify below some examples:

• Sungrow reninforces and reshapes its R&D investments to accelerate the PV business.

• Huawei is showing an impressive expansion with a penetration into diverse markets.

• BYD is following Toyota business model: the Chinese giant expands its activities towards the semiconductor industry

Under this context, what is the status of the Chinese supply chain? “Deeper you get on the inverter supply chain, less Chinese players exist,” comments Mattin Grao Txapartegi from Yole. Chinese companies such as CRRC, BYD, Goldwind… are leaders at the system level in many industries. At the power inverter level, the trend is different: they acquire technology competences by joint-ventures and acquisitions. “In the next 5-10 years, with the support of the government, they will get the know-how on the device level too”, adds Yole’s Analyst.

Share on:

Testimonial

"We’re proud to call I-Connect007 a trusted partner. Their innovative approach and industry insight made our podcast collaboration a success by connecting us with the right audience and delivering real results."

Julia McCaffrey - NCAB GroupSuggested Items

Simplifying Software Integration for Every Factory

10/22/2025 | Nolan Johnson, SMT007 MagazineAs a leading provider of factory digitalization solutions for electronics manufacturers, Cogiscan is at the heart of the software integration process. Davina McDonnell, director of marketing and product management, discusses how Cogiscan ensures that customers are ready to integrate and what it looks for to ensure a quick and appropriate installation.

MES Software Tools Need Thoughtful Integration

10/21/2025 | Nolan Johnson, SMT007 MagazineThe Global Electronics Association recently published a survey report on the state of EMS production software. This project, led by Thiago Guimaraes, director of industry intelligence, connects the dots across the global electronics value chain to uncover practical insights that individual companies might not have seen on their own. In this interview, Thiago discusses the whys and hows of this report.

SEMICON West: The Path to a $1 Trillion Future

10/14/2025 | Marcy LaRont, I-Connect007After more than 50 years in San Francisco, SEMICON West moved its 2025 show to Phoenix, which is significant because it highlights the importance of Arizona as a semiconductor and tech hub. Though the show will be back in San Francisco in 2026, the overwhelmingly warm welcome SEMI received from Arizona Governor Katie Hobbs, Phoenix Mayor Kate Gallego, and ASU President Michael Crowe—who has been responsible for ASU repeatedly achieving the U.S. News and World Reports most innovative university ranking—was remarked upon repeatedly. All indications are that SEMICON West may well be back in Phoenix after that 2026 season.

Technica USA Named Exclusive U.S. Distributor for DCT Cleaning Products

10/14/2025 | Technica USATechnica USA is pleased to announce a strategic partnership with DCT USA, LLC, becoming the exclusive master distributor of DCT cleaning products in the United States, effective November 1, 2025.

Is Glass Finally Coming of Age?

10/13/2025 | Nolan Johnson, I-Connect007Substrates, by definition, form the base of all electronic devices. Whether discussing silicon wafers for semiconductors, glass-and-epoxy materials in printed circuits, or the base of choice for interposers, all these materials function as substrates. While other substrates have come and gone, silicon and FR-4 have remained the de facto standards for the industry.